GMX ($GMX/$GLP) Overview: Pt. 1

GMX ($GMX/$GLP) Overview: Pt. 1

Your loss is my yield

Welcome to Elaborate VC! This will be part one of a two-part report about GMX that includes a summary of GMX’s functionalities and the protocols that are building on top of GMX, dubbed the “GLP Wars”.

Please share this newsletter if you think anyone else would benefit from reading it and feel free to share any thoughts with me about it via Twitter @Khrippex. Enjoy!

Statistics:

Total Funding: N/A

Stage: N/A

Investors: N/A

Current Team Size: Pseudonymous Team

Location: Remote

Website: gmx.io

History

GMX as we know it today was actually introduced as an interest-generating stablecoin (USDG) backed by leverage known as Gambit Protocol on February 26, 2021. Gambit officially went live on April 28, 2021, with USDG, XVIV, XLGE, xGMT, and GMT on BNB Smart Chain. However, in June 2021, a governance proposal was made and passed to consolidate the four tokens associated with Gambit, XVIV, XLGE, xGMT, and GMT, into a single GMX token before initiating a migration to Arbitrum on 22 June 2021.

To note, GMX tokens were initially converted and sold to the community at $2 a token, representing a 22x to the price of GMX as of this writing and a 31x to the ATH of GMX.

The migration to Arbitrum and the protocol known as Gambit concluded on July 6, 2021. On August 30, 2021, the rebranded GMX protocol released a launch plan that allowed the minting and redeeming of GLP tokens on September 1, 2021, and enabled GMX traders and trading on September 6, 2021. Furthermore, GMX launched on Avalanche on January 6, 2022.

About

GMX is a decentralized spot and perpetual exchange on Arbitrum and Avalanche. It allows users to swap between tokens like ETH, BTC, USDC, etc. but is primarily focused on its perpetual futures (perps) exchange product. Trading on GMX is supported by a unique multi-asset pool (GLP) and the platform earns revenue from liquidity providers fees from market making, swap fees, leverage trading (spreads, funding fees & liquidations) and asset rebalancing.

If you’re unsure about what a perpetual futures contract is, it is essentially a futures contract that has no contract settlement date. You can read more about it here and here.

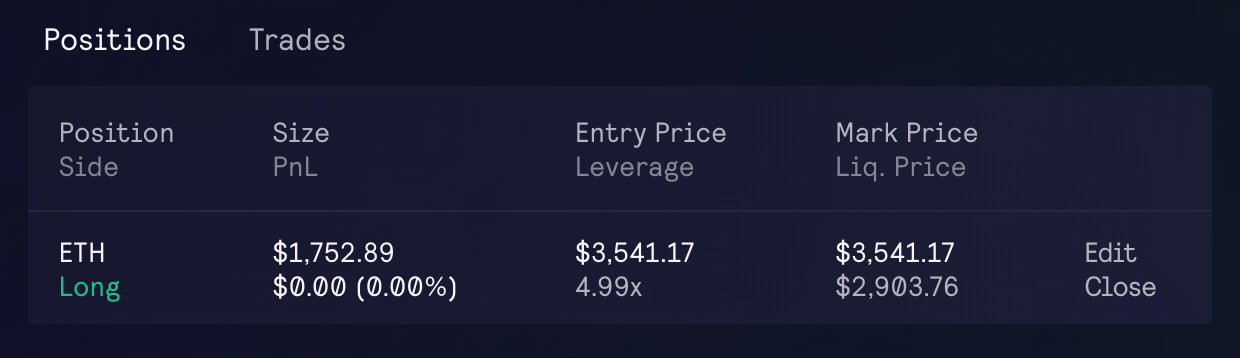

Trading perps on GMX instead of spot allows users to go long or short, trade on margin, and leverage their positions up to 50x. Trades are initiated by selecting a “Long” or “Short” position and selecting a base asset to pay in. Then the amount of leverage is chosen with a given “Entry Price” and “Liquidation Price” of the asset being bought. When opening a position, a snapshot of the USD price of your collateral is taken, so e.g. if your collateral is 0.1 ETH and the price of ETH is $3523.30 at the time, then your collateral is $352.33 and will not change even if the price of ETH changes.

Liquidation occurs when the amount of USD worth of tokens used as collateral to open the position is close to the loss amount. In the example above, the liquidation price would be where the paper loss amount nears $352.33. If this occurs, the trader’s collateral position would be taken by the protocol as revenue and distributed to GLP token holders and GMX token stakers in a 70/30 split.

“Real Yield”

GMX has been lauded by the crypto community as one of the only protocols that is able to consistently generate fees and therefore, “real yield” for its GMX and GLP token holders and stakers without the reliance on token inflation.

Since its launch in early September 2021, GMX has been able to consistently grow its total value locked (TVL) value to ~$475m as of writing and an additional ~$326m in value staked in the protocol.1 Through its increasing number of users and trading volume, it's been able to collect fees via liquidity providing and market making, swapping, asset rebalancing, and leverage trading (spreads, funding fees & liquidations).

An interesting source of revenue generated by GMX is its liquidations. When a trader has their position liquidated, GMX collects their collateral as revenue, so when traders lose, GMX wins and vice versa.

Users of GMX are able share in the revenue it generates by providing liquidity to traders through the purchases of GLP tokens or by staking GMX tokens. GLP token holders earn 70% of GMX's earned revenue while the other 30% of GMX's earned revenue is distributed to staked GMX token holders in ETH on Arbitrum or AVAX on Avalanche. As of writing, there is a total supply of ~476m GLP tokens at a price of $0.836, providing ~$398m worth of liquidity for traders on Arbitrum and a total supply of ~82m GLP tokens at a price of $0.674, providing ~$55m worth of liquidity for traders on Avalanche. There is currently a total supply of ~8.4m GMX tokens and 84% of the total supply of GMX tokens are staked in the protocol.2 GLP token holders are currently earning 20.17% APR on Arbitrum and 18.71% APR on Avalanche while staked GMX tokens are earning 12.84% APR on Arbitrum 12.74% APR on Avalanche.3

Due to reasons like GMX’s liquidity levels, ease of use, and UI, the platform has been able to consistently attract traders since its launch, even through events like LUNA/UST and FTX. Thus, they have been able to generate consistent fees, revenue, and yield for its liquidity providers and token stakers. This is what people in the community have been calling “real yield” because GMX has seem to found its product-market-fit and has become a mainstay in the crypto trading ecosystem.

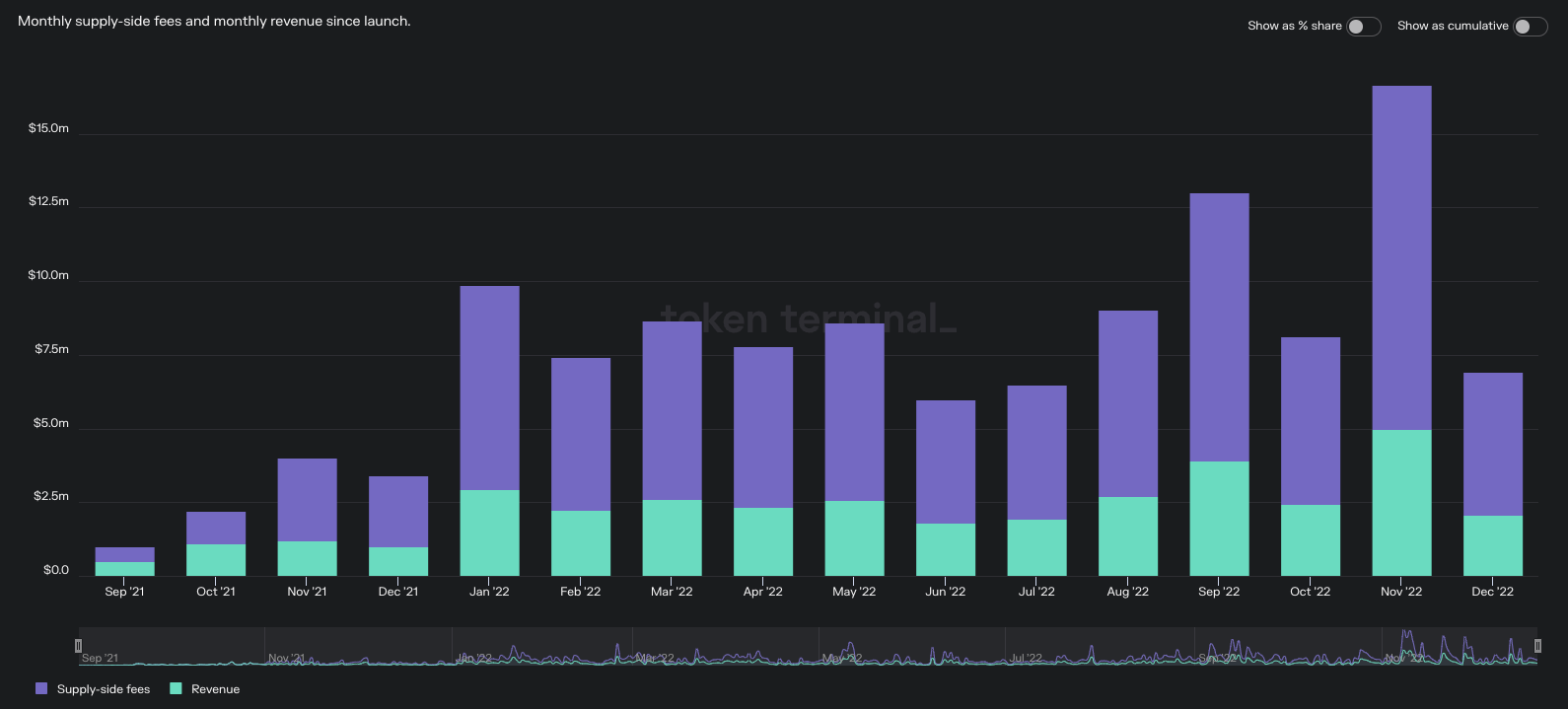

Below is a graph from Token Terminal displaying fees collected by GLP token holders (supply-side fees) and staked GMX token holders (revenue):

Token Terminal denotes supply-side fees as the portion of revenue that goes to liquidity providers or lenders and revenue as the portion of revenue that goes to token holders. They explain it here and here. Since 70% of revenue goes to liquidity providers or GLP token holders and 30% of revenue goes to GMX token stakers, you can see how the Token Terminal chart above is split 70/30.

Governance

GMX is governed by the GMX DAO, a relatively centralized DAO that relies solely on the core development team to introduce new proposals. Although GMX token holders can make suggestions to the protocol on the GMX DAO Forum page and vote on proposals with no minimum GMX holding, only six addresses identify as “Authors” and they are the only entities who can introduce new proposals. They are the following addresses:

0x5F799f365Fa8A2B60ac0429C48B153cA5a6f0Cf8 (Arbitrum / Avalanche)

0x6091646D0354b03DD1e9697D33A7341d8C93a6F5 (Arbitrum / Avalanche)

0xfb481D70f8d987c1AE3ADc90B7046e39eb6Ad64B (Arbitrum / Avalanche)

0xD7941C4Ca57a511F21853Bbc7FBF8149d5eCb398 (Arbitrum / Avalanche)

0x99Aa3D1b3259039E8cB4f0B33d0Cfd736e1Bf49E (Arbitrum / Avalanche)

0x82429089e7c86B7047b793A9E7E7311C93d2b7a6 (Arbitrum / Avalanche)

Tokenomics

GMX4: The GMX token is the native utility and governance token of the GMX protocol with a forecasted maximum supply of 13.25m tokens. The token allocation of GMX is as follows:

2 million GMX paired with ETH for liquidity on Uniswap.

2 million GMX reserved for vesting from Escrowed GMX rewards.

2 million GMX tokens to be managed by the floor price fund.

1 million GMX tokens reserved for marketing, partnerships and community developers.

250,000 GMX tokens distributed to contributors linearly over 2 years.

Any additional minting of GMX beyond the 13.25m max supply will be pushed through a governance vote to supply any new products if launched or if additional liquidity mining is required.

Utility

Governance: As stated previously in the Governance section, the GMX token is a governance token that allows holders to vote on governance proposals only.

Staking: The primary value-add function of the GMX token is the staking mechanism that gives stakers three types of rewards:

Escrowed GMX: These esGMX tokens are rewarded to stakers and can be converted into GMX tokens through a one year vesting period.

Multiplier Points: Multiplier points are rewarded to GMX stakers at a fixed rate of 100% APR, so 1000 GMX staked for one year will yield 1000 Multiplier Points. The Multiplier Points can then be staked for additional fee rewards:

Boost Percentage = 100 * (Staked Multiplier Points) / (Staked GMX + Staked esGMX)5

ETH / AVAX Rewards: 30% of revenue generated by GMX are distributed to GMX token stakers in ETH or AVAX depending on which network the GMX is staked on, Arbitrum or Avalanche.

The GMX token also has a floor price fund according to the GMX docs where they have partnered with OlympusDAO to own the GMX/ETH liquidity and provide Olympus bonds for GMX/ETH. The protocol can then generate revenue from the fees collected off of the GMX/ETH trading pair. The current floor price fund on Arbitrum and Avalanche stands at ~$2.6m and ~$2.5m respectively.

GLP6: The GLP token is the platform's "liquidity provider" token. It consists of an index of assets that is used to swap with and trade against during leveraged trading.

40.73% USDC

28.85% ETH

17.9% BTC

6.06% DAI

2.26% USDT

2.25% FRAX

1.14% LINK

0.77% UNI

37.97% USDC

27.63% BTC

18.02% ETH

6.5% WBTC

6.45% AVAX

3.39% USDC.e

GLP token holders earn 70% of the revenue generated by the GMX platform and can be minted and burnt using any index asset. The price for minting and redemption is calculated based on (total worth of assets in index including profits and losses of open positions) / (GLP supply). Fees for buying GLP will vary based on which assets the index has less or more of. You can view a price chart of GLP here since it isn’t on any traditional market information platforms.

Since traders on GMX essentially trade against the liquidity pool of GLP, it must be constantly rebalanced to back the most actively traded assets. For example, if the GLP index has a large percentage of ETH and a small percentage of USDC, actions which further increase the amount of ETH the index has will have a high fee while actions which reduces the amount of ETH the index has will have a low fee. Token weights are adjusted to help hedge GLP holders based on the open positions of traders. For example, if a lot of traders are long ETH, then ETH would have a higher token weight, if a lot of traders are short, then a higher token weight will be given to stablecoins.7

Risks

Surprisingly, GMX has been able to withstand the whirlwind that the year of 2022 has been for crypto, as revenue and TVL have been on an upward trend since the inception of GMX since September 2021.

Therefore, I don’t see larger systemic issues from crypto pose as much of a risk with GMX, but I do see limitations with regards to its liquidity structure and risk associated with its ability to fend off competitors.

@hodlKRYPTONITE highlighted a few reasons in his thread here on why he thinks GMX will fail. Since GMX traders trade against the GLP liquidity pool, the GLP liquidity pool can be left with massive exposure if there is a large drop in crypto prices while there is a large amount of short open interest (OI) on the platform. Since the GLP liquidity pool is made up of roughly 50% stables and 50% risk assets, the liquidity pool could dry up if ETH and BTC drop 50% in one day while the short OI profits massively in stablecoins, essentially draining and bankrupting the GLP pool. Although it isn’t common to see a 50% drop in asset prices, 2022 has clearly shown that tail end events can be a lot more common than previously thought. If an event like this occurred, GLP token holders, GMX stakers, and GMX would be in danger of running out of liquidity to make all users whole. The GMX team responded with counter measures against such a scenario here and further explained how @hodlKRYPTONITE proposed danger could never happen here. Other members have also tried explaining the situation here, here, and here.

@hodlKRYPTONITE mentioned an attack against GMX in his thread that occurred on September 17, 2022 at 01:07:19 UTC, on Avalanche. The attack happened against GMX’s AVAX/USD price oracle that resulted in estimated profits of $500k for the attacker. This occurred because even though GMX mentions that it uses Chainlink Oracles in its docs, GMX actually uses its own PriceFeed contract to fetch token prices from Binance, FTX, and Bitfinex and only uses Chainlink as a back-up oracle provider. Therefore, coordinated activity in those three exchanges on the trading pair, AVAX/USD, resulted in price manipulation and profit-taking from the attacker. Read more about the attack here.

Outside of GMX’s potential structural issues, GMX is clearly on the uptrend. However, I want to highlight the fact that there are no structural moats that GMX owns besides its current liquidity levels and brand that are continuing to keep traders on its platform. Due to the open-sourced nature of the protocol, anyone can theoretically fork its code and launch a copycat on any blockchain, even Arbitrum or Avalanche. We already see competitors like dYdX (DYDX), MUX Derivatives (MCB), and a relatively new protocol called Gains Network (GNX) that is planning to launch on Arbitrum soon.8 Even Synthetix (SNX) is launching a perpetual futures exchange called Decentrex on Optimism.

With competitors encroaching upon GMX from every side, it will be paramount for GMX to keep its traders on its platform to continue generating trading volume and revenue for the platform. As of now, besides its existing liquidity levels and brand, I’m not sure what will truly incentivize traders to stay as I believe that their product isn’t differentiated enough to keep traders on if competitors can create better UIs, UXes, or provide lower fees.

Competition

As stated above, GMX is a relatively generic perpetual exchange protocol that has many perpetual futures exchange competitors. Here is a preliminary list:

dYdX (DYDX)

MUX Derivatives (MCB)

Gains Network (GNX)

Decentrex (SNX)

Mycelium Perpetual Swaps (MYC)

Perpetual Protocol (PERP)

ApolloX (APX)

Deri Protocol (DERI)

As stated above, I believe competition will be a difficult area for GMX to contend to as more competitors join the space and attempt to steal GMX’s market share away, especially as I see no differentiating structural moat that protects GMX right now.

Concluding Remarks

Since GMX’s inception on Arbitrum in September 2021, it has clearly led the way as a sustainable crypto protocol that continues to attract traders, trading volume, and fees to its platform. As of writing, it dominates TVL figures on Arbitrum9 and also makes up a significant TVL figure on Avalanche.10 There was also a positively received proposal suggestion on the GMX DAO forum on November 23, 2022, by @_khanhamzah, the Head of DeFi at Polygon, to bring GMX to Polygon. As long as GMX is able to expand to other chains and continue to generate fees organically and consistently, it will remain as one of the only protocols that has managed to find product market fit and sustainability in a crypto market that’s been “rekt” over and over again. However, it will be increasingly more important for GMX to differentiate itself from new competitors to maintain the current traders on its platform and to attract new traders to sustain its growth. There lies a lot of execution risk that we will have to wait and see if the GMX team will be able to deliver on or not.

Overall, GMX has become an impressive protocol that has found its product-market fit and has continued to consistently generate revenue for the protocol and therefore, its liquidity providers and token stakers. Despite the risks mentioned, GMX has done a great job establishing itself as a decentralized destination for traders to trade perps. GMX gained additional attention after the collapse of FTX due to its decentralized and non-custodial nature. Despite the headwinds against the crypto industry as a whole, I believe GMX does have tailwinds as the largest decentralized perp exchange protocol with FTX’s collapse furthering its narrative as a non-custodial place for traders to trade. It will certainly be a protocol to keep an eye on, especially as we dive into Part 2 of this report, where we will be looking at the numerous protocols now building on top of GMX and specifically, its GLP token.

To learn more about GMX, I’d recommend reading @cosmo_jiang’s Twitter thread here and @ThorHartvigsen’s Twitter thread about GMX valuation here. You can also view all of GMX’s relevant pages, community projects, analytics dashboards, partnerships, and Telegram groups here.

I am not a financial advisor. The Content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice.